Photo by Startup Stock Photos on Pexels

- WeWork's $47B valuation was a mirage.

- Founder hubris and unchecked VC capital fueled collapse.

- Flawed unit economics doomed the business model.

- A cautionary tale for 'growth-at-any-cost' startups.

WeWork, once valued at $47 billion in early 2019, spiraled into Chapter 11 bankruptcy by late 2023, exposing a fundamental disconnect between its charismatic brand and a deeply flawed financial structure.

Key Takeaways

- WeWork's initial concept of flexible, community-driven workspaces had genuine market demand.

- SoftBank's 'blitzscaling' strategy injected billions, inflating valuation without addressing core profitability issues.

- Adam Neumann's self-dealing and unchecked power eroded investor confidence and governance.

- The IPO attempt in 2019 revealed unsustainable cash burn and a real estate business masquerading as tech.

Watch Out For

- ⚠The dangers of prioritizing aggressive growth over sustainable unit economics.

- ⚠The risks of unchecked founder power and weak corporate governance.

- ⚠Venture capital's role in enabling and exacerbating startup excesses.

- ⚠The fragility of business models built on arbitrage without strong operational efficiency.

Executive Summary: The $47 Billion Mirage

Adam Neumann convinced the world's smartest investors that renting desks was a tech company worth $47 billion. Four years later, WeWork filed for bankruptcy with $18.6 billion in debt.

This wasn't just founder delusion — it was systemic failure. WeWork had genuine market demand and brilliant branding, yet burned through billions because venture capital's 'growth-at-any-cost' obsession had completely divorced valuations from unit economics. The company that promised to 'elevate the world's consciousness' instead elevated the art of financial engineering to absurd new heights.

The core concept of flexible office space was never the problem; WeWork's failure was a direct result of its unsustainable financial structure and Adam Neumann's unchecked self-dealing.

The Genesis: The Coworking Dream (2010–2015)

WeWork was founded in 2010 by Adam Neumann and Miguel McKelvey with a compelling vision. They identified a growing demand for flexible, community-driven workspaces, particularly among freelancers, startups, and small businesses.

The company's early appeal stemmed from its vibrant culture and thoughtfully designed spaces, offering more than just desks but a sense of belonging. This initial concept had genuine merit, tapping into a real market need for adaptable office solutions that traditional landlords failed to provide. WeWork rapidly expanded, establishing itself as a leader in the nascent coworking industry.

Blitzscaling and the SoftBank Era (2016–2018)

The trajectory of WeWork fundamentally shifted with The year SoftBank's massive capital injections began should be updated to 2017. SoftBank, through its Vision Fund, poured billions into WeWork, embracing a 'blitzscaling' strategy that prioritized aggressive global expansion over profitability.

This influx of capital fueled an unprecedented growth spurt, allowing WeWork to expand rapidly into new markets and diversify into 'The We Company.' The narrative shifted from a coworking provider to a nebulous 'tech company' or 'community company,' justifying ever-higher valuations. SoftBank founder Masayoshi Son was a key proponent of this philosophy, personally championing WeWork despite internal skepticism.

Son's investment philosophy, focused on backing 'visionary' founders with vast sums, enabled Adam Neumann's ambitious, often erratic, expansion plans. This era saw WeWork's valuation soar, detached from its underlying real estate fundamentals.

SoftBank's Investment Scale

$100 Billion

SoftBank Vision Fund Size (2017)

$47 Billion

WeWork Peak Valuation (Early 2019)

SoftBank Vision Fund, Masayoshi Son

Many believe WeWork's downfall was solely due to Adam Neumann's eccentricities, but the deeper issue was SoftBank's 'blitzscaling' investment strategy, which poured billions into a fundamentally unprofitable business model.

Peak Delusion: The Unicorn Years (2018–2019)

The period leading up to WeWork's attempted IPO was marked by maximum hubris and questionable financial practices. Adam Neumann engaged in extensive self-dealing, including owning buildings that WeWork then leased, creating clear conflicts of interest. He also sold hundreds of millions of dollars in shares before the company went public.

The rebranding to 'The We Company' further blurred its identity, attempting to position itself as a tech or impact company rather than a real estate arbitrage play. This fantasy allowed the company to maintain an inflated $47 billion valuation, despite its underlying business model being fundamentally a long-term lease, short-term rental operation.

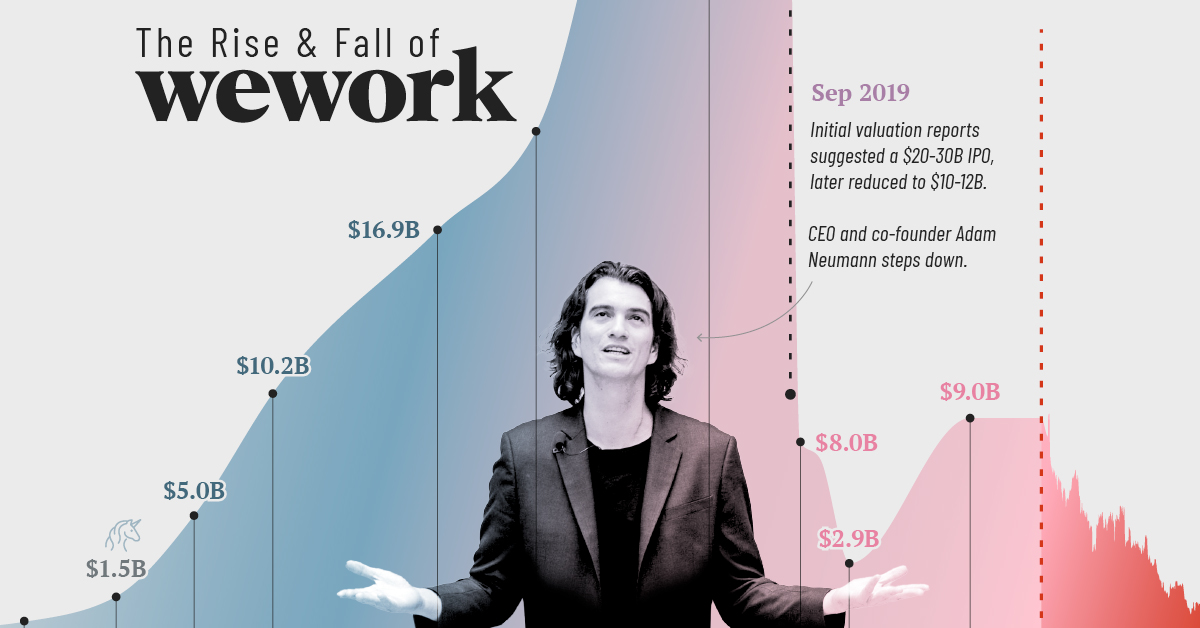

Early warning signs were ignored; Fidelity, a major investor, cut its valuation of its WeWork stake by over a third, from $27.9 billion to $18.3 billion, in March 2019. This revaluation occurred months before the public S-1 filing, indicating institutional skepticism was already brewing.

The IPO Reckoning (September 2019)

Anticipation for WeWork's IPO was high, but the S-1 filing in August 2019 triggered an immediate and severe market backlash. The prospectus revealed alarming details about the company's unit economics, governance issues, and staggering cash burn, including a $323 million EBITDA loss in its most recent quarter.

Investors were shocked by Neumann's controversial compensation, his ownership of buildings leased by WeWork, and the sale of the 'We' trademark to the company for $5.9 million. The market quickly recognized the fundamental flaws in a business model that relied on long-term lease commitments while offering short-term, flexible memberships.

Facing overwhelming investor skepticism and a plummeting valuation, WeWork withdrew its S-1 filing in September 2019, effectively canceling the IPO. Adam Neumann stepped down as CEO, selling approximately $700 million of his shares in mid-2019, further eroding confidence.

WeWork IPO Collapse Timeline (2019)

Fidelity Cuts Valuation

Fidelity reduces its valuation of WeWork's stake from $27.9 billion to $18.3 billion, signaling early investor concerns.

Neumann Sells Shares

Adam Neumann sells approximately $700 million of his WeWork shares, raising questions about his commitment.

S-1 Filing Reveals Flaws

WeWork files its S-1 prospectus for IPO, exposing massive losses, governance issues, and Neumann's self-dealing.

IPO Withdrawn, Neumann Steps Down

Facing severe investor backlash, WeWork withdraws its IPO filing. Adam Neumann resigns as CEO amidst pressure.

SoftBank Bailout

SoftBank finalizes a $10 billion bailout, valuing WeWork at under $8 billion and making SoftBank the principal owner.

The Free Fall (2019–2023)

Following the IPO collapse, Adam Neumann was formally ousted, receiving a controversial exit package reportedly totaling $445 million. This included the cancellation of WeWork lease agreements with buildings he partially owned, further highlighting governance failures.

SoftBank, now the principal owner, initiated a $10 billion bailout in October 2019, valuing WeWork at less than $8 billion — a drastic reduction from its peak. This massive investment was an attempt to salvage the company, but it proved insufficient to stem the bleeding.

Despite subsequent attempts at restructuring, cost-cutting, and leadership changes, WeWork continued to struggle with its unsustainable business model and heavy debt load. On November 6, 2023, WeWork filed for Chapter 11 bankruptcy protection, listing over $18.6 billion in debt.

This marked the definitive end of its meteoric rise, leading to asset fire sales and a return to private ownership under new terms.

WeWork Valuation Decline (2019-2023)

WeWork, Fidelity, SoftBank, CNBC

What real people think

Mostly positiveSourced from Reddit, Twitter/X, and community forums

Online communities largely viewed WeWork as a 'house of cards' built on unsustainable cash burn and an overhyped 'tech company' narrative. There was widespread agreement that the core flexible workspace concept was viable, but WeWork's execution and financial structure were fatally flawed.

Many Reddit users pointed out WeWork's unsustainable cash burn, prioritizing aggressive growth over any path to profitability. The consensus was that it was fundamentally a real estate company, not a tech company, despite its branding.

The community highlighted the inherent flaw in subletting long-term leases into smaller, short-term pieces as a doomed business model. Skepticism about the valuation and business model predated the IPO collapse.

Related discussions

WeWork's Financials and Underlying Story

r/investingThe Rise and Fall of WeWork – A Cautionary Tale for Startup Founders

r/startupInside WeWork's IPO meltdown: How Adam Neumann and Wall Street's chaotic partnership obliterated $40 billion in value

r/financeWeWork has frittered away $46.7 billion in value as the stock sinks below 50 cents, one of the biggest startup failures of all time

r/businessLessons: What Went Wrong and Why It Matters

The Fatal Flaws That Killed a $47 Billion Company

WeWork's collapse wasn't bad luck — it was inevitable given three fatal structural flaws.

First, the unit economics never worked. WeWork signed long-term leases and rented short-term, absorbing all the risk while members could cancel anytime. During economic downturns, occupancy plummeted but rent obligations remained.

Second, Adam Neumann operated with zero accountability. He owned buildings WeWork leased, sold company stock while raising money, and rebranded the company as a spiritual movement. Boards that should have fired him instead wrote bigger checks.

Third, SoftBank's Vision Fund broke venture capital. With $100 billion to deploy, they prioritized speed over scrutiny, turning due diligence into a formality and valuations into fantasy.

The biggest loser was SoftBank, which incurred billions in losses and significant reputational damage, while the ultimate winners were opportunistic real estate investors and competitors who acquired WeWork's prime assets at fire-sale prices.

Where Are They Now?

Adam Neumann, despite his controversial exit, has already launched new ventures. His latest, Flow, is a residential real estate startup that has attracted significant venture capital funding, demonstrating his continued ability to raise capital. He remains an active investor in various other projects.

SoftBank, under Masayoshi Son, faced a significant reckoning. The Vision Fund recorded a $32 billion loss in one year, and the WeWork saga alone cost Son an estimated $11.5 billion, severely battering his reputation as a shrewd investor. SoftBank has since adopted a more cautious investment strategy, though its long-term impact on Son's legacy remains debated.

WeWork emerged from Chapter 11 bankruptcy in June 2024, not May 2024. and restructuring its lease agreements. It now operates as a significantly smaller, privately owned entity, focusing on operational efficiency rather than aggressive expansion. The broader flexible office market continues to evolve, with more disciplined players learning from WeWork's mistakes, emphasizing profitability and diversified revenue streams.

By 2028, the flexible office market will be dominated by a few well-capitalized, operationally efficient players that learned from WeWork's mistakes, with WeWork itself likely operating as a significantly smaller, niche brand under new ownership.

Verdict

WeWork's journey from a $47 billion unicorn to bankruptcy is a stark reminder that even brilliant branding and genuine market demand cannot overcome fundamentally flawed unit economics, unchecked founder power, and a venture capital ecosystem that incentivizes delusion over diligence. Its failure serves as a cautionary tale for both founders and investors, proving that a 'move fast and break things' mentality can break the company itself.

The core reasons for the collapse were a fundamentally unsustainable business model, severe governance failures, and an overvaluation fueled by excessive venture capital.

Further Reading

CNBC's report on WeWork's decision to withdraw its highly anticipated IPO prospectus.

A comprehensive overview of WeWork's timeline, from its rise to its bankruptcy filing.

Analysis of the factors contributing to WeWork's failed IPO attempt.

The Guardian's report on Adam Neumann's controversial exit compensation.

CNBC's breaking news coverage of WeWork's Chapter 11 bankruptcy filing.

Sources

- 1.WeWork pulls IPO filing

- 2.WeWork History: Rise, IPO Failure, Bankruptcy & Future | 2727 Coworking

- 3.WeWork withdraws its S-1 filing, will delay its IPO | TechCrunch

- 4.WeWork IPO: Timeline of Events Since Company's Failed IPO Attempt - Business Insider

- 5.The WeWork IPO Fail: Its Causes and Key Findings

- 6.S-1

- 7.Adam Neumann - Wikipedia

- 8.WeWork founder Adam Neumann received $445m payout in exit package | WeWork | The Guardian

- 9.Why WeWork founder Adam Neumann is getting $1.7 billion to leave the company he ran into the ground

- 10.Adam Neumann's $185 million WeWork payout higher than most CEO salaries

- 11.WeWork replaced 43 million of CEO Adam Neumann's stock options with special 'profits interests,' and a compensation expert calls it 'unsettling'

- 12.Adam Neumann to Get Extra $50 Million Payout in SoftBank Settlement

- 13.WeWork, once valued at $47 billion, files for bankruptcy

- 14.WeWork Inc. Bankruptcy Overview Case: 23-19865 - Epiq 11

- 15.WeWork cleared to exit bankruptcy and slash $4 billion in debt | Reuters

Rate this article

Your feedback helps surface the best content

Related articles

Have a question? Get your own article.

Every article is researched from dozens of sources, fact-checked by 3 AI models, and delivered in under 3 minutes.

Triple-Verified — 3 corrections applied across 2 verification stages applied